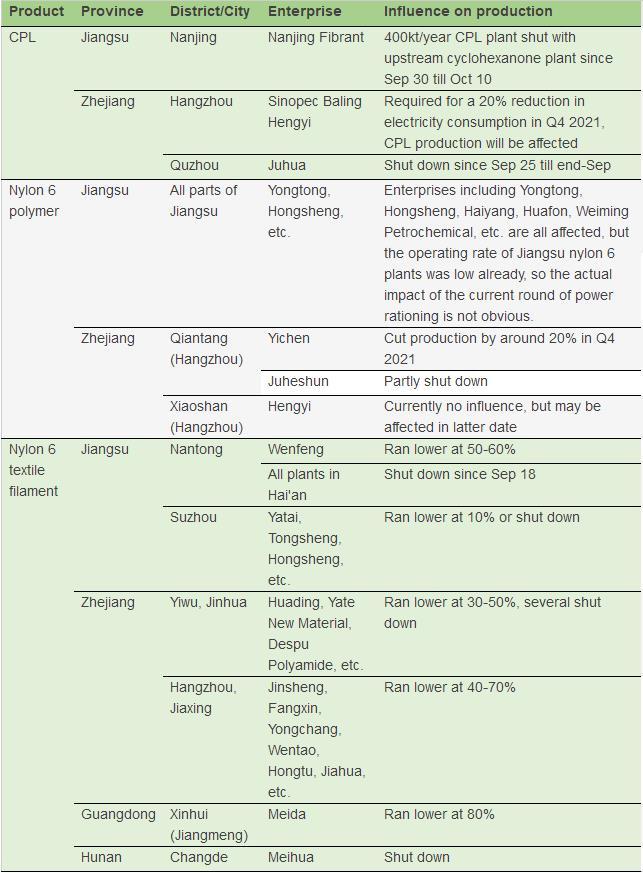

Influence of “dual control” on CPL and nylon 6 industry

The“Dual Controls”on energy consumption and energy intensity–or the amount of energy consumed per unit of GDP, have exerted impacts on the operating rate of all industries to various degrees. Nylon 6 industrial chain, from caprolactam, to nylon 6 polymer, textile filament and downstream weaving and knitting factories are all affected. By September 29, the operation changes along the industry have been summarized in below figure.

Figure 1. Impart of“dual controls”on plant operations in nylon 6 industry

The "Dual-Control" target refers to the energy consumption intensity ("energy consumption per unit of GDP") and total energy consumption. The energy consumption per unit of GDP of 2021 is aimed at about 3% this year. But more than half of the provinces failed to achieve the goal of controlling energy consumption and intensity in the first half of the year.

CPL: supply tight, still price may fall

To briefly summarize the market operation in September, CPL market has been driven up by still tight supply-demand structure and the quickly rising benzene cost. We had mentioned at the end of August that CPL would be still tight in September. In Sep, downstream nylon 6 HS chip demand was not good due to the weak performance of textile end. But nylon 6 CS chip market trading had several rounds of expansions, especially the high-viscosity CS chip, which was boosted by industrial filament and cord fabric plants.

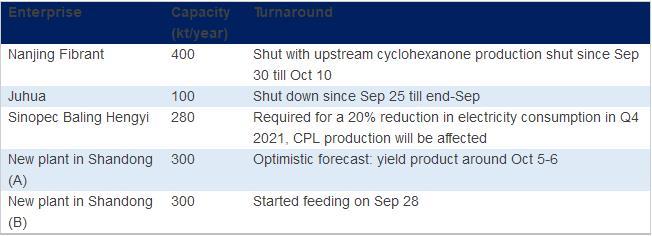

Figure 2. CPL plant turnaround and start-up plans in near future

The supply and demand structure of CPL market is still expected to be tight in October 2021, despite of two new plants (total of 600kt/year) expected to be start up in the month. First, the operating rate of the newly started will be limited at low, and this time line (listed in above figure) is still possible to be postponed. Second, the restock in downstream nylon 6 polymer plants is extremely low, and polymer plants still need to replenish certain amount of feedstock to ensure normal production. And polymer plants’rigid demand may expand narrowly, as it had been restricted by low-operation due to the continuous tight supply of CPL since Aug. Once the tension is certainly to be eased, polymer plants may ramp up their operating rate. Above all, the supply and demand relation is still favorable for CPL sellers.

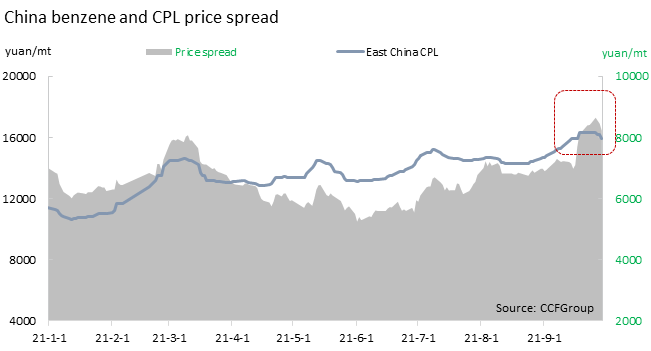

However, tight supply may not support CPL uptrend further in Oct.

First, from downstream side, downstream price increase could not catch up. The Sep contract settlement for CPL was 1,200yuan/mt higher on the month, which is evidently beyond nylon textile filament market increase. On the non-textile side, CS chip trading has expanded, while transactions at higher prices are limited, which means the actual traded level has not lifted as much as CPL. Therefore, it is very hard for CPL contract settlement to rise further in Oct.

Second, the pressure on benzene market is huge in Oct. Benzene prices have been rising significantly in Sep, while a large part of the driving force is from speculators. In Oct, as Zhejiang Petrochemical begins to supply to the market, and import arrivals increase evidently, benzene prices may be further pressure down. And as its downstream sectors have all been impacted by the dual control policy, benzene fundamentals are looking more bearish. Conservatively speaking, the Oct contract settlement for benzene may come down by over 500yuan/mt month-on-month to below 7,500yuan/mt.

Furthermore, current CPL-benzene price spread is high above 8,000yuan/mt, the marginal effect of cost driving force is much weaker than previous months.

A most likely scenario is that CPL market may be temporarily steady in H1 Oct, and price may start adjusting narrowly since mid-Oct when the new capacity release and influence of dual controls become clearer.

There is only tiny possibility for CPL prices to rise up, when CPL supply is evidently reduced due to the dual controls, and textile industry recovers evidently in Oct. But this is not likely based on current observation. CCFGroup holds that CPL sellers may yield marginal profit to downstream even when the supply-demand structure remains tight in Oct.

Nylon 6 chip: operation mainly steady, CS chip demand healthy

The operating rate is basically steady among nylon 6 polymer makers. Only several plants in Zhejiang and Jiangsu are affected, while the curtailment is not evident. Polymer makers in Jiangsu including Yongtong, Hongsheng, Haiyang, Huafon, Weiming Petrochemical, etc. are all affected, but the operating rate of Jiangsu nylon 6 plants was low already, so the actual impact of the current round of power rationing is not obvious. By the end of Sep, the operating rate of nylon 6 HS chip plants pegs at 73% and that of CS chip plants stands low at 58%.

Demand for nylon 6 CS chip has been improving since September, mainly due to recovering industrial-grade use and modified plastic consumption. Demand for high-viscosity CS chip has been very hot. And the chip shortage which curbs automobile production is expected to ease in the last quarter of 2021, and that will be a benefit to the consumption nylon-based modified plastics.

In comparison, the condition in nylon 6 HS chip market is not as good as players expect for the traditional peak season. Downstream textile filament sales are largely restricted by both power rational and high inventory burden. And the dual control policy has affected the weaving and knitting mills evidently as well (to be discussed in the following part). Even the dull-grade HS chip sector, which has been performing very good in the first half of 2021, is gradually losing edge.

NFY and downstream are affected to different degrees

Since mid-September, weaving, knitting and dyeing factories in major textile bases have reduced production. At the same time, nylon filament yarn producers have reduced or stopped operation to varying degrees, and the average operating rate of the industry has dropped significantly.

1. Weaving and knitting mills may keep low run rate in Oct

Starting from mid-Sep, Shaoxing, Yiwu (Zhejiang), Wujiang (Jiangsu), Chaoshan, Dongguan (Guangdong) and other regions have gradually implemented the dual control policy, and weaving factories have reduced and stopped production.

For example, more than 160 textile-related enterprises in the Keqiao Binhai Industrial Park in Shaoxing (Zhejiang) have all stopped; the dyeing industry in Wujiang have largely been suspended for holiday; production is generally restricted in Yiwu, and so on. Since mid-Sep, the average operating rate of Zhejiang circular knitting machines and Guangdong warp knitting devices has generally dropped by 5-10%, while that of Wujiang water jet looms has dropped by 55%.

The production restriction will be ended by the end of Sep, however, the week-long holiday in Oct may still affect a certain part of weaving and knitting plants, who have not received enough orders. Their production shutdown may be extended. It is probable that the recovery in weaving and knitting mills’operation after the National Day holiday (Oct 1-7) will be limited, and they may keep running at low-capacity for a period of time.

2. Operation of NFY plants

The dual control policy also has varying degrees of impact on the production of nylon texitle filament plants. The average operating rate of NFY plants has dropped from 85% in late Aug to 71% in end Sep. The influence is mainly focusing on Zhejiang and Jiangsu province (East China), while Fujian (South China) is so far not evidently affected.

Jiangsu province: Local POY and DTY plants in Hai’an are all closed except Wenfeng, which si now running at 50-60%. So the region’s average load is less than 10%. Wuxi area has no direct impact. NFY plants in Changshu, Wujiang are required to shut or curtail production for 3 days, and some have already closed or curtailed production to below 70%.

Zhejiang province: Yiwu and Jiaxing silk mills dropped to around 6.5-7.5%, and some 40%. NFY mills in Zhuji, Xiaoshan, Yuyao and other regions have also received power rationing notices, but there are no specific measures. Most companies are running steadily, with individual mills reducing production actively based on the order taking and inventory condition, by 10-20%. Major plants are running at 70-80%, and some are at 90% or 50%.

Fujian province: No power rationing requirements are received yet. Mainstream medium and large manufacturers mostly run at 90-95%. However, there are also 2-3 NFY factories curtail production to 70% or below due to their downstream customers’production cut or shut.

So far, both nylon filament and downstream weaving and knitting plants are still confused about the dual control policy, as the specific measures are changing according to actual effect. So their operating rate may also be adjusted flexibly in the latter period. Some players have a cautious-to-positive outlook toward market after the production limit, while the possible decline in CPL market makes their opinion more prudent.

the latter period. Some players have a cautious-to-positive outlook toward market after the production limit, while the possible decline in CPL market makes their opinion more prudent.

ave a cautious-to-positive outlook toward market after the production limit, while the possible decline in CPL market makes their opinion more prudent.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price