PX grapples with strong fundamentals but weak expectation

Recently, polyester chain seems to have entered consolidation, in the lack of a clear direction. PX fundamentals are currently strong, but the expectation is weak.

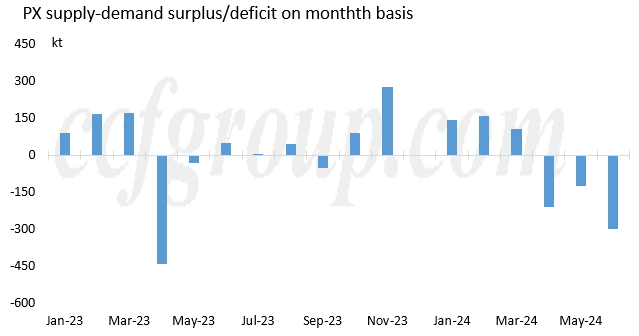

1. Continuous inventory reduction

With Asian PX plants beginning turnaround season since Apr, China PX inventory started reducing continuously. During Apr and May, the inventory decreased by a combined amount of more than 300kt in China, and in Jun, it is estimated to further decline by 300kt.

On overall basis, China PX inventory is likely to drop by about 600kt in the second quarter, which could offset the increase since Nov last year. Therefore, the high inventory pressure would get relieved, which would be supportive to PX price.

2. Expectation of increasing supply

Trading in PX spot market is currently centering on Jul and Aug goods, and after the rollover of laycans next week, the trading would be centering on Aug and Sep goods. Then, PX would be challenged by expectation of rising inventory again.

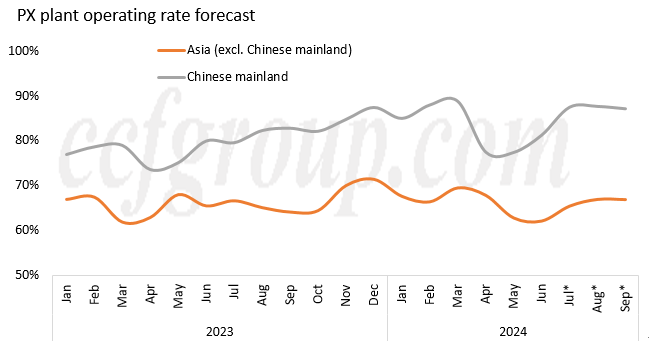

On supply front, the turnaround season for Asian PX plants began in late Mar, and would approach the end gradually in Jun. With several plants restarting in mid or late Jun, China PX plant operating rate is recovering. According to CCFGroup's investigation, plants with combined capacity of 10.37 million mt/yr would restart in Jun, while plants with combined capacity of 3.56 million mt/yr are under maintenance during the same period.

|

Company |

Location |

Capacity (kt/yr) |

Turnaround |

|

|

Supply increase |

Zhongjin |

China |

1600 |

Apr 16 – Jun 7 |

|

Weilian Chemical |

China |

2000 |

May 11 – late Jun |

|

|

Sinopec Fujian |

China |

1000 |

O/R up by 5-10% in Jun |

|

|

Hengli |

China |

2500 |

May 23 – early Jun |

|

|

Fuhaichuang |

China |

800 |

May 20 – end-Jun |

|

|

Idemitsu |

Japan |

400 |

Apr 29 – late Jun |

|

|

ENEOS |

Japan |

350 |

Late Feb – end-Jun |

|

|

Hanwha Total |

South Korea |

770 |

Apr 25 – late Jun |

|

|

SK |

South Korea |

400 |

Early May – mid-Jun |

|

|

GS |

South Korea |

550 |

Feb 26 – Jun 5 |

|

|

Supply reduction |

Hengyi Brunei |

Brunei |

1500 |

O/R cut to 70% in end-May |

|

Rabigh |

Saudi Arabia |

1340 |

Shut in mid-May |

|

|

FCFC |

Taiwan, China |

720 |

T/a from early Jul for 45 days |

Based on the schedule, the monthly average of China PX plant operating rate is estimated to rise to above 87% in the third quarter, up by 8-9 percentage points. And the Asian operating rate outside China is likely to tick up by 2 percentage points.

The operating rate is anticipated to recover to the level in the first quarter, while that in Asia would still be 1-2 percentage points lower.

In addition, US gasoline stocks increase, while gasoline to crude oil price spread narrows. As a result, Asia to US aromatcis price spread has been squeezed rapidly since mid-May. Asian MX price declined in tandem, and PX-MX price spread has recovered to above $90/mt on FOB Korea basis. The spread on Chinese yuan basis has also widened. If the spread further enlarges, some PX units based on MX could hike operating rates, and then the average run rate of PX would further move up.

Market participants are concerned that the situation in the first quarter with backlogs of inventory and big discount of spots to formula pricing could repeat in the third quarter.

3. Mixed expectation on demand

Earlier in the first quarter, polyester inventory was increasing gradually from low to high, and the impact on plant operating rate was limited. Currently, polyester inventory hovers on the high side and the economics are poor, raising concerns about production cuts.

As for PTA, the production is expected to increase in the third quarter compared to the first quarter. FCFC Ningbo and Sinopec Yizheng started their new PTA plants in end-Mar and Apr, Hanbang restarted its plant in end-May and Pengwei also plans to restart its PTA plant. Though downstream polyester is weighed by high inventory, PTA production may still increase.

In addition, in the first quarter, PX suppliers were under pressure from low ratio of contract as well as high inventory, and had to turn to selling in spot market. But after the contract ratio has increased and PX inventory has reduced in the second quarter, the pressure has been alleviated for most suppliers. However, buying intentions in USD goods from China domestic buyers is affected by the big difference between CNY/USD selling rate and central parity rate.

In a conclusion, in the third quarter, with maintenance completing and PX-MX spread widening, China and Asian PX production would increase obviously, and PX inventory would rise again. However, the increment could be smaller than that in the first quarter with the growth of downstream demand. Selling pressure has been relieved after inventory reduction in the second quarter. Therefore, any downward space for PX price would be limited, unless polyester plant operating rate is cut sharply. Any rebound in PX price would also be curbed due to high inventory of polyester, poor economics as well as the upcoming power rationing on polyester plants. In the near term, PX market is expected to continue the consolidation.

|

Company |

Location |

Capacity (kt/yr) |

Turnaround |

|

|

Supply increase |

Zhongjin |

China |

1600 |

Apr 16 – Jun 7 |

|

Weilian Chemical |

China |

2000 |

May 11 – late Jun |

|

|

Sinopec Fujian |

China |

1000 |

O/R up by 5-10% in Jun |

|

|

Hengli |

China |

2500 |

May 23 – early Jun |

|

|

Fuhaichuang |

China |

800 |

May 20 – end-Jun |

|

|

Idemitsu |

Japan |

400 |

Apr 29 – late Jun |

|

|

ENEOS |

Japan |

350 |

Late Feb – end-Jun |

|

|

Hanwha Total |

South Korea |

770 |

Apr 25 – late Jun |

|

|

SK |

South Korea |

400 |

Early May – mid-Jun |

|

|

GS |

South Korea |

550 |

Feb 26 – Jun 5 |

|

|

Supply reduction |

Hengyi Brunei |

Brunei |

1500 |

O/R cut to 70% in end-May |

|

Rabigh |

Saudi Arabia |

1340 |

Shut in mid-May |

|

|

FCFC |

Taiwan, China |

720 |

T/a from early Jul for 45 days |

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price