PX pressured by PTA plant shutdown

PX price pulled back on Sep 27 to $912/mt CFR, down $4/mt from previous trading day, despite that upstream crude oil and naphtha hiked, and downstream PTA and polyester rose.

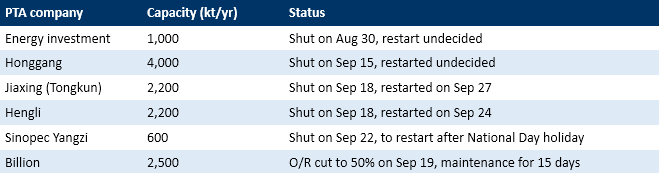

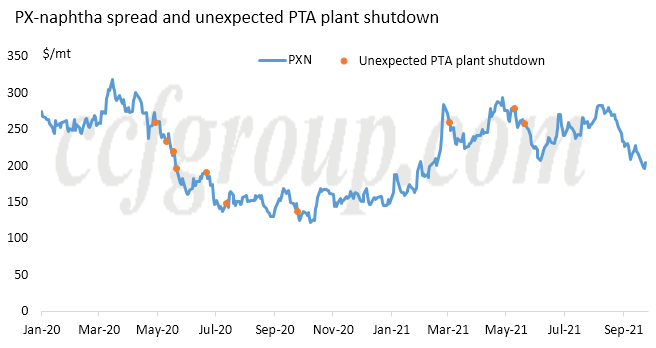

In the morning trading session on Sep 27, bids for PX spots were at $927/mt CFR, but then, discussion sentiment softened at noon, and bids for Nov goods were down to $913/mt CFR in the close session. The restart of Honggang’s PTA plant was undecided, and could be delayed until after National Day holiday, hence some Oct PX contracts were cancelled. As a result, PX spot market was weighed with the contango between Nov and Dec widened to $2.5/mt. PX-naphtha spread was also squeezed to below $190/mt, new low since Feb 2021.

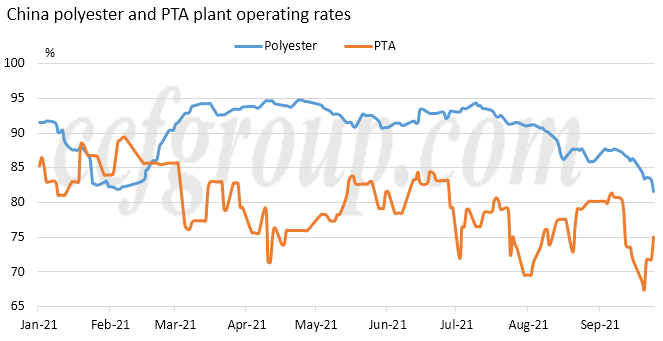

With China stepping up dual controls on energy consumption and intensity, polyester chain has been affected. In addition, several PTA plants shut unexpectedly or cut operating rates in Sep. Both PTA and polyester plant operating rate declined heavily.

Though PTA operating rate has recovered slightly, it is still around this year’s low level. Polyester operating rate has dropped to approach the low point during the Spring Festival, and may refresh this year’s low if the dual controls deepens.

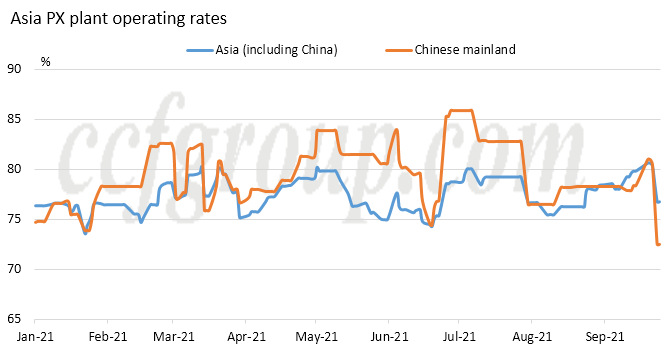

China PX operating rate declined sharply as well recently, as Hengli Petrochemical and Fuhjia Dahua shut their plants for scheduled maintenance. However, as China relies on large amount of PX imports, and the shipments are arranged in advance, hence the unexpected shutdowns of PTA plants and extended duration of shutdowns could lead to a sudden increase in spot PX supply and even shortage of storage space for PX. Therefore, PX market could be under greater pressure.

That situation repeated more than once last year. In May 2020, several unplanned shutdowns of PTA plants in China led to squeeze of PX-naphtha spread.

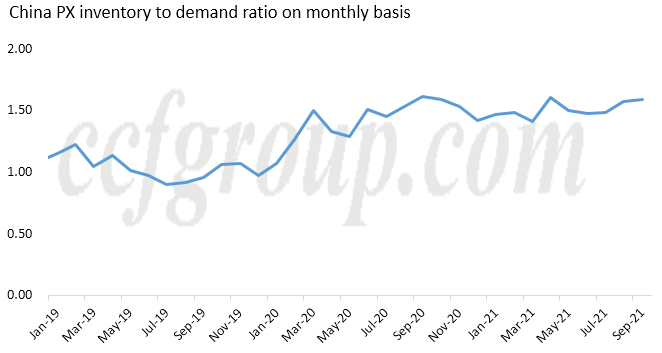

The reason behind it is that China’s PX self-sufficiency rate has increased, and China PX inventory maintains high. Once the demand shrinks unexpectedly, limited commercial tanks for PX could hardly provide a cushion and suppliers, strained by oversupply, have to lower prices, leading to fast squeeze of PX-naphtha spread.

Therefore, the force majeure on Honggang’s PTA plant impacts PX market obviously. Looking forward, the end-use and polyester plant operations would continue to be affected by the dual controls. As for PTA, though the operating rate recover with plants restarting and processing margin increase, it would be difficult for the operating rate to rise substantially due to maintenance schedules and subdued demand from polyester. As for PX, PX-naphtha spread may remain low. PX price may track the movements of feedstock, but further changes would be dependent on the impact from dual controls.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price