Styrene market enters a cycle of losses and low inventories

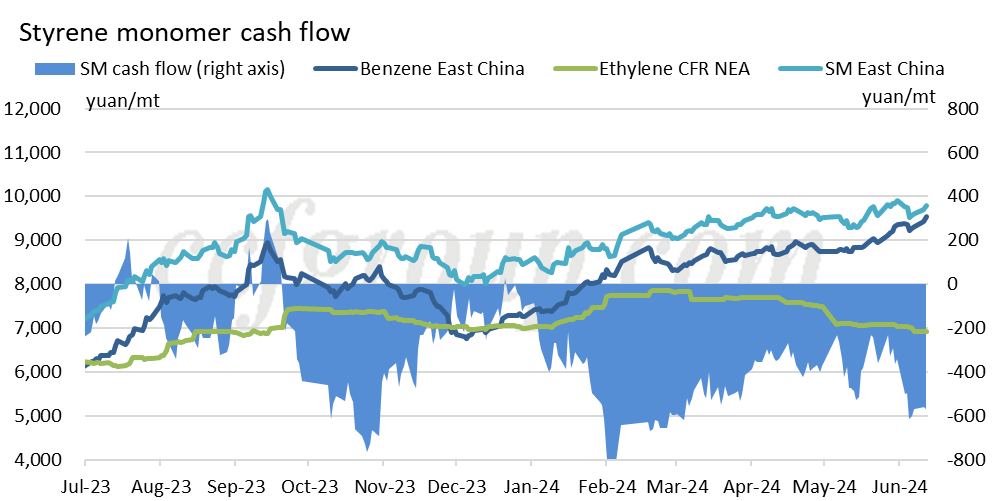

Since the beginning of the month, styrene prices have slightly rebounded, maintaining a relatively high level for the year. However, the styrene industry continues to face expanding losses, affecting long-term supply, with strong downstream resistance to high prices, resulting in stagnant trading activity. The spot price difference between styrene and benzene has narrowed to 230yuan/mt, a historically low level.

| Company | Location | Capacity,kt/yr | Turnaround/Status |

| PetroChina Dushanzi | Xinjiang | 360 | t/a mid-May, 2 months |

| Tianli Petrochemical | Xinjiang | 40 | t/a mid-May, 2 months |

| North Huajin Chemical | Liaoning | 177 | t/a Jul, 55 days |

| ChemChina Huaxing Chemical | Shandong | 80 | shut on Jun 14 |

| Zhejiang Petroleum & Chemical | Zhejiang | 600 | Jun 12, 2 weeks |

| Dagu Chemical | Tianjin | 500 | Aug, 45 days |

| Lihuayi | Shandong | 720 | may cut rate |

| Haiwan Chemical | Shandong | 500 | Jul, 45 days |

| Zibo Junchen | Shandong | 500 | cut to 70% |

| Jiaxi Chemical | Anhui | 350 | cut to 70% |

| Satellite Petrochemical | Jiangsu | 600 | cut to 70% |

| SP Chemicals | Jiangsu | 320 | cut to 70% |

| New Solar Chemical | Jiangsu | 350 | may cut rate |

The strong benzene market is squeezing cash flow in downstream industries, impacting the stability of styrene plant operations. Routine maintenance and increased rate cuts are affecting non-integrated units purchasing outsourced benzene, keeping the styrene industry operating below 70%. Zhongtai Chemical's 600kt/year styrene unit is scheduled for trial runs by the end of July, with production depending on profitability. Additionally, Ineos Styrolution's 430,000 mt/year styrene unit in Sarnia, Canada, which was temporarily shut down due to environmental issues, announced a permanent closure by June 2026. Increased production from Chinese styrene units is impacting North American styrene exports. The compressed styrene-benzene spread suggests that styrene supply growth will be much lower than expected, leading to reduced styrene inventories.

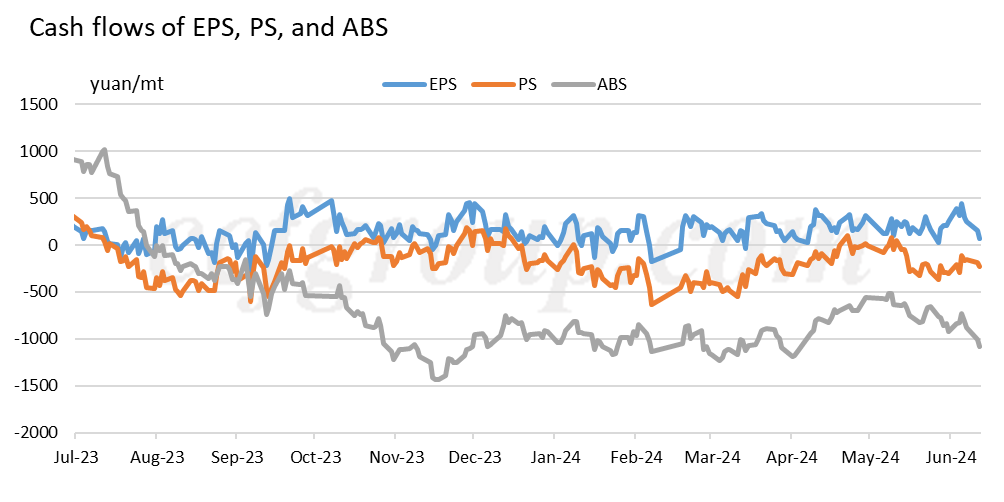

Styrene's profitability closely aligns with downstream ABS/PS sectors, particularly affecting cash flow. ZPC's 400kt/year ABS unit has reached full capacity, and its second phase 1.2 million mt/year ABS unit is set for phased commissioning in July. The joint production of styrene and downstream PS/ABS strains the industry's profitability. In contrast, independent EPS units have seen slower new capacity additions in recent years, maintaining positive cash flow and steadily increasing operating rates.

The pricing power within the styrene industry chain heavily depends on benzene. The entire chain, including styrene and downstream ABS/PS, is currently operating at a loss, caught in a cycle of declining profits and inventories. The situation is unlikely to improve until there is a reduction in medium and small capacities and slower new capacity additions, alleviating short to medium-term losses.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price