China's PFY export may grow in H2 2022

China's PFY exports amounted to 1,628kt in Jan-Jun, 2022, down 0.3% on the year, which were at 781kt in Q1, down 13.5% on annual basis, and at 847kt in Q2, up by 16.1% year on year. Export surged in May and Jun.

As for the second half of year, PFY export is likely to apparently increase in Q3 2022 with low volume in Q3 2021. Exports are likely to increase over the same period of last year in Q4, while the increment may be not obvious. The total PFY exports are estimated to be at 3.15 million tons, a year-on-year rise of 5.1%.

Although some orders of textiles were mentioned to be rerouted from China to Southeast Asia, exports of PFY to Asia dropped the most apparently. The proportion of Asia decreased to 59.4% from 62.4%, that of Europe and Africa inched down, and that of South America rose the most (especially Brazil), up to 12.1% from 9.4%, followed by North America.

| Exports of PFY by variety in H1 of 2021-2022 (Unit: tons) | ||||

| Variety | H1 2021 | Proportion | H1 2022 | Proportion |

| POY (54024600) | 354553 | 21.70% | 258412 | 15.90% |

| FDY (54024700) | 290855 | 17.80% | 257445 | 15.80% |

| DTY (54023310) | 660004 | 40.40% | 783046 | 48.10% |

| PIY (54022000) | 284984 | 17.50% | 277976 | 17.10% |

| Textured yarn (54023390) | 32352 | 2.00% | 39880 | 2.40% |

| Other PFY (54025200) | 9776 | 0.60% | 11053 | 0.70% |

Exports of DTY outshined in the first half of 2022, with proportion up to around 50%, while those of POY and FDY witnessed negative growth. Export of POY decreased by near 30% year on year. It was cheaper to directly purchase DTY instead of buying POY this year. In addition, export increase mainly came from some garment processing nations (like Pakistan), while these regions are not integrated with DTY capacity, which further intensified the divergence of exported varieties.

| Top 10 export destinations of PFY in H1 of 2021 and 2022 (Unit: tons) | ||||

| Destination | H1 2021 | Proportion | H1 2022 | Proportion |

| Pakistan | 132660 | 8.10% | 175545 | 10.80% |

| Vietnam | 144945 | 8.90% | 154978 | 9.50% |

| Egypt | 142767 | 8.70% | 139764 | 8.60% |

| Brazil | 109783 | 6.70% | 138566 | 8.50% |

| Turkey | 157351 | 9.60% | 136653 | 8.40% |

| India | 217063 | 13.30% | 116478 | 7.20% |

| South Korea | 111529 | 6.80% | 105131 | 6.50% |

| Bangladesh | 78131 | 4.80% | 77850 | 4.80% |

| Indonesia | 54351 | 3.30% | 66589 | 4.10% |

| Mexico | 34073 | 2.10% | 47501 | 2.90% |

Exports to India collapsed this year after skyrocketing in 2021, with export volume to India down by above 100kt in H1 2022. Soaring exports to Pakistan and Brazil failed to make up the losses in India, which was one of the major reasons for diving proportion of Asia.

One thing should be noted: Brazil market may have pulled forward some demand in the second half of 2022. It was heard that Brazil will levy anti-dumping duty on DTY from China, and cargos that reach Brazil before end-Aug will be waived the ADD, while the specific duty rate still needs further confirmation. Pakistani rupee has been plummeted, greatly impacting its import and export.

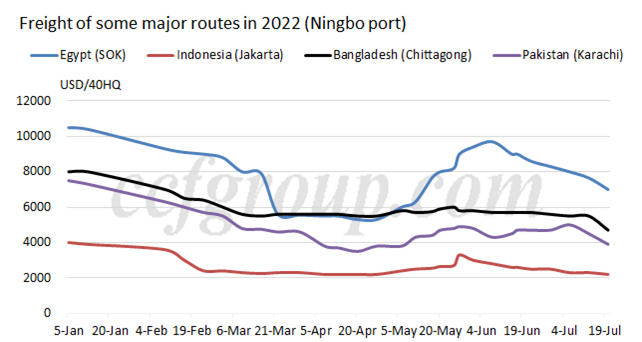

The freight from Ningbo port to Brazil/NAV rose to US$11,000/40HQ, at US$10,500/40HQ in actual trading, which was at US$7000/40HQ in early-Jun. The freight of the Red Sea route fell. The freight from Ningbo to to Egypt/ SOK dropped to US$7,000/40HQ, which may be at US$6,700/40HQ next week and was at above US$9,000/40HQ. The freight to Pakistan/Karachi was at US$3,900/40HQ and that to Indonesia/Jakarta reduced to US$2,300/40HQ.

The freight of South America route extended higher since Jun and that of other routes was in downward consolidation. The reduction tends to accelerate this week and next week. As many routes have abundant shipping space, many market players expect the freight to keep reducing in the second half of year.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price