Pressure on PX reduces with demand recovering

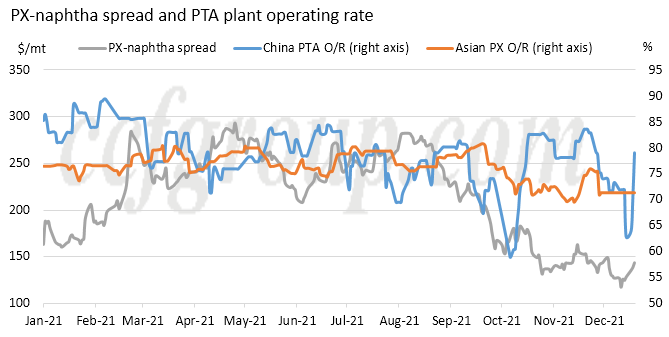

PX profits have been squeezed rapidly since late Nov, with PX-naphtha spread narrowing from $163/mt to below $120/mt in mid-Dec, hitting record low. This round of squeeze in PX-naphtha spread was closely related to the sharp drop in PTA plant operating rate in China. PX was dragged down by weaker demand.

However, the demand is expected to rebound.

Since late Nov, adding to the low margins, some unexpected plant issues occurred and the pandemic re-surged in Zhejiang Province, leading to sharp decline in PTA plant operating rate which fell from the high point of 84% to 63% in mid-Dec. Afterwards, with supply and demand improving, PTA margin recovered some losses, with its spread to PX rebounding from 400yuan/mt to the current level of 600yuan/mt. With acetic acid cost included, PX margin has rebounded from 180yuan/mt in mid-Nov to the current level of 390yuan/mt.

With PTA margin improving, pandemic situation alleviating, and maintenance completing, some PTA plants are getting restarted.

| Company | PTA capacity (kt/yr) | Status |

| Fuhua | 4500 | O/R cut to 80% on Nov 24, up 90% |

| Billion | 2500 | Shut on Dec 1, restarted on Dec 19 |

| Yisheng Dalian | 6000 | Shut unexpectedly on Dec 17, restarted |

| Yisheng New Materials | 3600 | O/R cut to 30% on Dec 7, up to 90% |

| INEOS | 1100 | To shut in mid-Dec for 2 weeks |

| OPSC | 750 | Shut on Dec 2 for maintenance, to restart in end-Dec |

| Shenghong | 2500 | Shut unexpectedly in end-Nov, to H1 Jan |

Therefore, China PTA operating rate is expected to rebound to 82% in early Jan, and may further increase to 84% after Shenghong restarts its plant. Meanwhile, no PTA producer has announced maintenance plan in Jan yet.

On supply front, Sinopec HRCC (Hainan Refining) plans to shut its 1 million mt/yr PX plant in end-Dec for maintenance till H1 May 2022, and shut its 660kt/yr PX plant in H2 Feb for 2-month maintenance. Meanwhile, Sinopec Fujian is poised to restart its PX plant in mid-Jan and expand the capacity by 150kt/yr to 1 million mt/yr. Sinochem Quanzhou is slated to restart its 800kt/yr plant in late Jan. Zhejiang Petroleum and Chemical is expected to complete maintenance on its 2 million mt/yr line in end-Dec. Zhongjin Petrochemical may have maintenance schedule, but the date is undecided. In addition, Sinopec Yangtze could start maintenance in end-Feb, Aromatics Malaysia plans to shut its 550kt/yr PX plant in Jan-Feb 2022 for maintenance, Oman Aromatics’plant is scheduled to start maintenance in end-Dec 2021.

In a conclusion, with PTA operating rate rising, the impact from Shenghong’s PTA plant shutdown has winded down, and the pressure on PX has relieved. As PTA margin is in negative territory, PX-naphtha spread may recover some losses. There could still be pressure from PX plants’raising operating rates and restarts, and demand from PTA could be affected by polyester and end-use plant operating rate cuts prior to the spring festival starting from end-Jan.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price