Polyester and downstream market outlook after the Spring Festival

Before the Spring Festival, downstream demand was better than market expectations. Coupled with a rebound in raw materials, there was a relatively significant rebound in prices of polyester products. For example, the price of POY increased by 600-700yuan/mt and the profitability notably restored.

In the month leading up to the Spring Festival, the operation of downstream sector was better than market expectations for several reasons. Firstly, there was still good export demand at the end of the year. In the U.S., there was a rush for exports as downstream customers required that Chinese goods be shipped before New Year's Day to ensure they arrived in the U.S. before Trump took office. Secondly, the Muslim Ramadan is expected to begin on March 1, 2025, just after the Chinese New Year, prompting some orders to be completed and shipped before the holiday. According to customs data, China's textile and apparel exports in December reached $28.069 billion, an increase of 11.1% year-on-year, driven by the rush for exports.

Secondly, the low absolute prices increased downstream players' tolerance for finished product inventories, especially as some water-jet fabric manufacturing clusters maintained high operating rates before the holiday, actively accumulating inventory in anticipation of favorable market conditions in the first half of the year. As a result, statistics of CCFGroup showed that the inventory of grey fabrics were about a week higher than the same period of last year and the changes in downstream inventory should be noted, which may affect operating rates.

During the Spring Festival, news regarding the downstream market included the U.S. imposing additional tariffs on Chinese goods. Starting from 12:01 AM (Eastern Time) on February 4, 2025, an additional 10% tariff will be levied on all goods originating from China and Hong Kong. This tariff policy has no exemptions, meaning that small import packages valued under $800 will also be taxed. This will significantly impact cross-border e-commerce, as since 2018, under the backdrop of the U.S.-China trade war, packages valued below $800 have been exempt from tariffs, allowing many cross-border e-commerce products to enter the U.S. market duty-free.

Although the imposition of these tariffs was somewhat anticipated, the market had already speculated multiple times before the holiday about the potential for increased tariffs after Trump took office. However, this situation differs from previous instances.

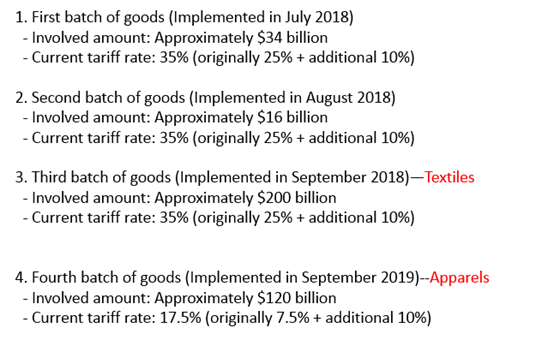

In the past, the U.S. Department of Commerce and the Office of the Trade Representative needed to conduct investigations before the president could decide on imposing tariffs based on the findings. For example, from the initiation of the 301 investigation against China in August 2017 to the implementation of the 301 tariffs in April 2018, it took over six months, allowing time for a rush of exports.

This time, Trump has invoked the International Emergency Economic Powers Act, allowing him to directly impose tariffs. As a result, the tariffs took effect immediately without leaving time for a rush of exports, which may weaken the anticipated rush for exports in the first half of the year.

Currently, feedback from customers making U.S. orders indicates that after Trump announced the 10% tariff on China, prices for post-holiday orders are being renegotiated, with both parties needing to share the burden of the increased tariffs. For instance, Chinese sellers might bear 5%, while U.S. buyers take on the other 5%. The increased costs from the tariffs are forcing some low-margin orders to be lost, or some U.S. buyers are shifting their orders elsewhere. Therefore, after the tariffs are imposed, the proportion of exports to the U.S. may further decline.

However, since 2018, export data showed that the U.S.-China trade war has not adversely affected the quantity of textile and apparel exports. Although traditional markets like Europe, the U.S. and Japan have declined, China has expanded its exports through the Belt and Road Initiative and investments in ASEAN countries, resulting in an overall increase in export volume, albeit with a downward trend in export prices and profits.

Overall, it is believed the impact of the U.S. imposing a 10% tariff can be summarized in several points: 1. The proportion of exports to the U.S. is expected to decline further. 2. Due to the immediate implementation of the tariffs, the rush for exports may be significantly weaker than expected. 3. In the short term, there may be a drag on exports, but currency devaluation and potential policy support for exporting enterprises may offset some of the tariff impacts. In the medium to long term, the overall impact on export volume will be limited (with a decrease in apparel exports and an increase in fabric and raw material exports), but it will intensify competition in the export profit. 4. The taxes increase on small imported packages worth less than $800 will suppress the growth momentum of cross-border e-commerce exports.

After the Spring Festival holiday, most DTY plants and fabric mills will restart operation near Feb 5-13 and the normal operating rate may appear until after Feb 13 after workers returned to work.

Compared to last year, the resumption of downstream production was relatively positive for two reasons: 1. For knitting enterprises, the domestic demand at the end of 2023 was strong, and the inventories were nearly cleared. With low inventory, the resumption of work in knitting sector was quite active after the holiday, even though orders were weak, the operating rate remained high. 2. Weaving enterprises had good business in the first half of 2024, and the inventory reduction was quite evident, especially in the Changxing, where there were even instances of sold-out situations. With high operating rate in knitting and weaving mills, the overall operating rate of DTY plants and fabric mills hit multi-year high in Zhejiang and Jiangsu.

This year, based on current market observations, some knitting fabric plants have relatively high inventories, coupled with fewer new orders. The enthusiasm for resuming work after the holiday appears to be mediocre, with feedback from Changshu and Haining indicating that the operating rate may be lower than the same period of last year. In weaving fabric sector, there is some differentiation; reports suggested that the Changxing area received many orders before the holiday, and the resumption of work after the holiday is expected to be smooth. However, since many have already built up inventory before the holiday, the actual performance may fall short of market expectations. In contrast, the Wujiang area is expected to perform worse than Changxing, as there is a significant amount of inventory left over from the previous year's good sales of certain fabrics. Overall, it is believed that the pace of production resumption in the downstream sector after the holiday may not match last year's levels.

During the Spring Festival, the prices of polyester products, including filament, staple fiber and PET bottle chip remained stable. However, the market entered a holiday mode, with limited transactions. Most polyester companies ceased sales from Lunar New Year's Eve to the fifth day of the New Year, resuming sales gradually on the sixth day (Feb 3). After the holiday, prices of polyester products are anticipated to be largely stable in short run. If feedstock price remains weak after holiday, price of polyester products is likely to slightly decline with high processing spread.

Regarding inventory, for example, the inventory of POY was near 13 days before the Spring Festival holiday and was estimated to be around 19 days by Feb 4 based on operating rate (specific statistics would be confirmed after the holiday), which was lower than the same period of last year. Both upstream and downstream players have stockpiled, with statistics showing an average stockpile of just over 20 days. In the two weeks following the holiday, the inventory of PFY is anticipated to be under uptrend.

From the perspective of the polyester market in 2025, the new capacity and output of polyester filament and staple fiber are relatively limited. Cautiously optimistic view is held toward the recovery of profitability for these two products, while the supply of PET bottle chip is still significant and its profitability is expected to remain low.

As for the polyester polymerization rate, some units restarted operation or had turnaround during the Spring Festival holiday. The polyester polymerization rate increased limitedly on Feb 4, estimated to be 79.6%, up by one percentage point over pre-holiday level. The production resumption was slightly slower than the previous anticipation. More units will restart production from Feb 5 and the rise of run rate may accelerate. However, as some plants may delay restarting, the average polyester polymerization rate in February is estimated to be slightly lower than the earlier estimate 87%, and the average run rate of January is expected to be 84%.

Additionally, it is planned that 3 million tons of polyester facilities will restart in March, with the remaining facilities restarting in February. The operating rate is expected to peak in March, but the average rate in April may be slightly higher than in March. Furthermore, in March and April, there will be a 600kt/year boiler renovation project by Rongsheng and a 400kt/year relocation project by Hengyi, both expected to restart in the second quarter. Therefore, the polyester polymerization rate is expected to be 91.5% in March and at 93% in April, with adjustments made based on actual demand.

The main variables affecting polyester polymerization rate in the future will still be in PET bottle chips, as the production of filament and staple fiber has been limited in recent years. After the Spring Festival, the operating rate is not expected to be low, while the pressure on PET bottle chips remains significant. Additionally, this year, there are pressures from the production of 1500kt/year at Sanfangxiang, 500kt/year at Sinopec Yizheng and 600kt/year at Fuhai, which will continue to exert pressure on the operating rate of PET bottle chip plants.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price