PX and PTA markets during Chinese New Year and the outlook

| Product | Market | 2025-01-27 | 2025-01-28 | 2025-01-29 | 2025-01-30 | 2025-01-31 | 2025-02-03 | Feb 3/Jan 27 change | Unit |

| WTI | 73.17 | 73.77 | 72.62 | 72.73 | 72.53 | 73.16 | -0.01 | $/b | |

| Brent | 77.08 | 77.49 | 76.58 | 76.87 | 76.76 | 75.96 | -1.12 | $/b | |

| USD/CNY | central parity rate | 7.1698 | / | / | / | / | / | / | |

| Naphtha | CFR Japan | 676 | 669 | / | / | 665 | 657 | -19 | $/mt |

| Naphtha | FOB Singapore | 73 | 72 | / | / | 72 | 71 | -2 | $/b |

| Isomer-MX | FOB Korea | 770 | 768 | / | / | 768 | 770 | 0 | $/mt |

| Isomer-MX | CFR China | 790 | 788 | / | / | 788 | 790 | 0 | $/mt |

| Isomer-MX | CIF Rdam | 835 | 837 | 846 | 849 | 844 | 857 | 22 | $/mt |

| Isomer-MX | FOB USGC | 284 | 284 | 284 | 284 | 285 | 285 | 1 | cts/gal |

| Isomer-MX | FOB USGC | 866 | 866 | 866 | 866 | 869 | 869 | 3 | $/mt |

| Paraxylene | FOB Korea | 842 | 838 | / | / | 836 | 844 | 2 | $/mt |

| Paraxylene | CFR Taiwan | 863 | 859 | / | / | 857 | 865 | 2 | $/mt |

| Paraxylene | FOB Rotterdam | 870 | 870 | 870 | 870 | 870 | 870 | 0 | $/mt |

| Paraxylene | FOB USGC | 921 | 918 | 918 | 918 | 915 | 924 | 2 | $/mt |

Feedstock prices were little changed from Jan 27 to Feb 3, during Chinese New Year holiday.

WTI crude oil futures fell slightly by $0.01/bbl during that period. Although Brent crude oil price seemed to fall slightly more, by $1.12/bbl, it was mainly attributed to the rollover of most active contract month from March to April. As for the April contract, the price decline was only $0.22/bbl. During the holiday, Brent crude oil fluctuated in the range of $72-75/bbl. Compared with the pre-holiday pullback, the fall slowed down.

Trump's tariff policy triggered market fluctuations. The Federal Reserve kept interest rates unchanged. EIA data showed that US crude oil inventories increased as of January 21. In addition, OPEC+ planned to gradually increase oil production since April and abandon using EIA data also affected oil prices.

Naphtha prices fell by $19/mt to $657/mt on Feb 3 compared with Jan 27, and naphtha to crude oil price spread remained around $85/mt. Although olefin to naphtha spread widened slightly, it was around $200/mt, still indicating losses, curbing demand for naphtha in Asia. In addition, gasoline consumption was basically stable, and the overall purchase of naphtha was on need-only basis. MX was relatively strong and stayed stable, with FOB Korea price at around $770/mt and CFR China price at $790/mt.

As for PX, the price was up slightly by $2/mt over the same period to $865/mt CFR China on Feb 3, and it was also attributed to the rollover the laycans.

|

Date |

Seller |

Buyer |

Price ($/mt) |

Delivery month |

Source |

|

2025/1/28 |

HENGLI |

GSCX |

864 |

Apr |

Near-haul |

|

2025/1/28 |

TOTALSG |

GRAFIGURA |

863 |

Apr |

Near-haul |

|

2025/1/31 |

BPSG |

GSCX |

862 |

Apr |

Near-haul |

|

2025/1/31 |

BPSG |

SKGC SG |

862 |

Apr |

Near-haul |

|

2025/2/3 |

Glencore |

BPSG |

860 |

Mar |

Near-haul |

|

2025/2/4 |

HENGLI |

BPSG |

853 |

Mar |

Near-haul |

|

2025/2/4 |

Glencore |

GSCX |

854 |

Mar |

Near-haul |

|

2025/2/4 |

TOTALSG |

SKGC SG |

860 |

Apr |

Near-haul |

Selling and buying intentions were little changed during the holiday. As of Feb 4, discussion for Mar spots was at $12/mt discount to formula pricing, Apr goods at $8/mt discount, and May goods at $6/mt discount. Mar/Apr spread widened from -$4/mt to -$8/mt.

PX-naphtha price spread widened slightly, up by 11% from $188/mt before the holiday to $209/mt on Feb 3, indicating underwhelming economics. PX-MX price spread hovered low, at around $75/mt, indicating losses for PX units based on MX.

In terms of plant operations, China PX plant operating rate was quite stable. Fujia Dahua's 1.4 mln mt/yr PX lines cut operating rate slightly to 80%, while CNOOC Huizhou's operating rate recovered slightly by 5 percentage points to 95%. Outside China, Japan's ENEOS shut its 350kt/yr PX line in end-Jan for scheduled maintenance lasting 45 days.

South Korea exported about 372.9kt of PX in Jan 2025, down 83.8kt from the month earlier, data showed. About 307.9kt of the exports went to Chinese mainland, down 69.1kt on month; 20.5kt to Taiwan, down 49.7kt on month; and 44.5kt to the US, up 35kt on month.

Outlook

There is no plant maintenance in Feb announced in China, while plants including Sinopec Jiujiang, CNOOC Huizhou, Sinopec Yangtze and Sinopec Tianjin have announced maintenance plans in Mar-Apr. In addition, the schedule of ZPC and Weilian Chemical should be paid attention to.

Outside China, South Korea's GS and Japan's ENEOS have plant maintenance in Feb. In Mar, there could be no maintenance. However, in Apr, plants such as ENEOS, Malaysia Aromatics, PetroRabigh, and Taiwan's FCFC, with combined PX capacity of 2.4 mln mt/yr would undergo maintenance.

Therefore, PX supply and demand are expected to improved gradually, with inventory expected to increase by 100kt in Jan-Feb, little changed in Mar, but reduce by more than 200kt in Apr.

The outlook of PX is expected to turn upbeat, but near-term PTA plant operations should be watched closely.

PTA

PTA price assessment was suspended during the holiday. The price could be little changed from the perspective of cost.

Before the holiday, one 2 mln mt/yr PTA line in East China was shut for maintenance, and the restart date was undecided. One 3.6 mln mt/yr PTA line in East China got restarted on Jan 27, kept operating rate at 50%, and whether it would raise run rate would be depending on demand. One 1.25 mln mt/yr PTA line in South China was shut on Jan 12. China PTA plant operating rate was assessed at about 80% as of Feb 4.

China PTA inventory increased by 400~450kt in Jan, owing to polyester production cuts prior to Chinese New Year holiday. During the holiday, PTA inventory further rose, because of logistics restrictions, and slow buying from polyester plants. After the holiday, the arrivals of PTA goods to the ports are expected to increase obviously, and then the inventory could accumulate.

Outlook

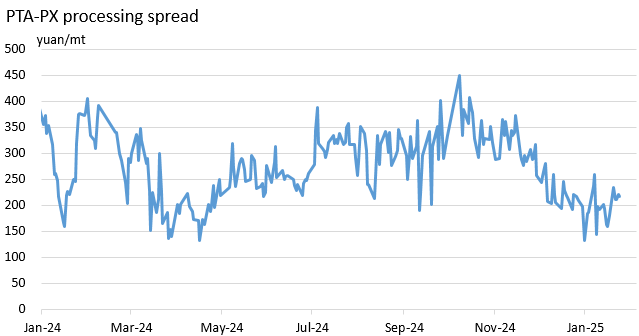

PTA-PX processing spread is currently meager, at merely 210yuan/mt, indicating poor economics, which could restrict plant operating rate.

PTA-PX processing spread= RMB PTA spot - PX CFR China/Taiwan * 0.655 * 1.02 * 1.13 *Exchange rate selling price (yuan/mt)

On demand side, China polyester plant operating rate could be slightly lower than earlier expected, at around 87% in Feb, but then it could rebound to 92-93% in Mar-Apr. As for PTA, the average operating rate is estimated at 86-87% in Feb, but may drop to 85% in Mar, and hover at 85-86% in Apr, based on daily production / (domestic PTA capacity / 365). Yisheng Ningbo and Yisheng New Materials keep low operating rates; Yisheng Hainan, INEOS, Yisheng Dalian, Sinopec Yizheng, Energy and Investment, Jiatong and Billion could undergo maintenance in Feb-Apr. In addition, Hengli Dalian's two PTA lines could undergo maintenance, as the maintenance plan was not implemented last year.

It is expected that PTA will continue to accumulate inventory in January and February, totaling around 700,000 to 800,000 tons. However, inventory will be reduced in March and April, with a total of around 450,000 tons. Therefore, PTA may improve in March and April, but considering the total accumulated inventory of over 900,000 tons from December 2024 to February 2025, and the current stock of over 1.1 million tons in the futures delivery warehouse, PTA prices are likely to remain under pressure in the later stages.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price