Nylon filament to enter a peak expansion phase

After several years of slow capacity growth, the application of nylon filament yarn (NYF) has expanded in the past two years, leading to a significant increase in demand. This has resulted in frequent occurrences of tight supply across multiple specifications, with profits generally rising. In this industry context, numerous new projects are emerging, and the industry is set to enter a peak expansion phase.

According to CCFGroup statistics, the currently approved nylon 6 textile filament projects have a combined capacity exceeding 2 million tons per yarn, with an expected increase of 400,000 to 450,000 tons/year in 2024. In 2025, an additional capacity of over 1 million tons/year is planned. However, the rapid expansion of capacity may lead to a situation where demand cannot absorb the supply immediately, and it is anticipated that a considerable portion of the planned projects will be delayed until 2026 or later.

1. New NFY projects categorized by enterprise type:

| Type of enterprise | Companies with NFY expansion projects include: |

| Leading enterprises' expansion | HSCC, Eversun Jinjiang, Huading Nylon, Jiahua |

| Fabric enterprises extending into filament industry | Shantou: Shengda'an, Yinghua, Jinshi, Tianhao; Quanzhou: Xiangxing Textile; Siyang: Yangyue, etc. |

| Raw material integrating with filament production | Saning, Fangyuan, Shenma, Yuehua New Materials, etc. |

| Expansion of established factories | Xinlun, Xinsen, Fujian Kaibang, Yongchang, Century Star, Hongtu, Tongsheng, Jianda, Hubei Zhongjin, etc. |

| Cross-industry investment | Yousheng, Nanshan Zhishang, Hecheng Jianeng, Meigaoxin Materials, Hongcheng, Jiayuan, etc. |

Many of the planned NFY projects focus on improving the industrial chain or continuing to expand scale. For example, established factories in the industry are expanding, and downstream weaving and knitting or upstream raw materials are extending into the textile filament segment. Weaving and knitting factories primarily use nylon filament equipment for their own use, including circular knitting machines in Shantou, warp knitting in Fujian, and jet looms in Jiangsu. However, a small number of manufacturers are already planning for the second and third phases in the future, leveraging their geographical advantages to shift from self-use to external sales.

Companies related to nylon industry continue to expand, driven by optimism in demand for nylon, the need for industrial layout, and the desire to enhance corporate risk resistance and profitability. However, some companies, originally involved in polyester, clothing, and integrated trade, despite lacking a foundation in the nylon industry, still have high expectations for it and are entering the nylon sector from other industries.

2. New projects by regional distribution:

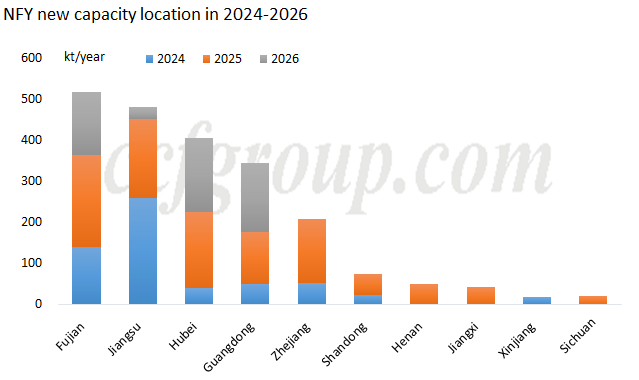

The numerous new capacities are not only expanding in industrial bases like Fujian, Zhejiang, and Jiangsu but also achieving breakthroughs or high growth in regions like Hubei, Jiangxi, Xinjiang, and Sichuan, where nylon filament factories were previously rare.

The new projects in 2024 are mainly concentrated in North Jiangsu, including companies like Jiahua, Huaze, and Guchuang. Fujian is also seeing expansion primarily from established factories, while new capacity distribution in other regions is relatively balanced.

In 2025-2026, there will be a large number of projects launched in Hubei, Fujian, Guangdong, Jiangsu, and Zhejiang. Hubei and North Jiangsu, with advantages such as low land and electricity costs, strong local government support, and good development momentum in weaving, knitting, and clothing industries, will see a clustering of new projects. As a result, Hubei will quickly become one of the main production areas.

Moreover, with new capacities emerging in a wide span of regions, the industry's concentration will temporarily decline. However, as competition intensifies, leading enterprises will still maintain their competitive edge for further expansion under their integrated advantages, leading to a rebound in industry concentration. Furthermore, the new capacities in 2024-2025 will primarily focus on FDY, indicating that competition in FDY will heat up earlier; while the release of new capacities for POY and DTY will occur relatively later, it is expected that the supply-demand structure for FDY will be slightly better in the next 1-2 years.

For more detailed information on industrial expansion and progress, please refer to the September research report "Emerging Nylon Filament Industry Clusters Gradually Taking Shape" and "2025 Nylon Outlook Report."

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price