Recent direct-spun PSF fundamental data overview

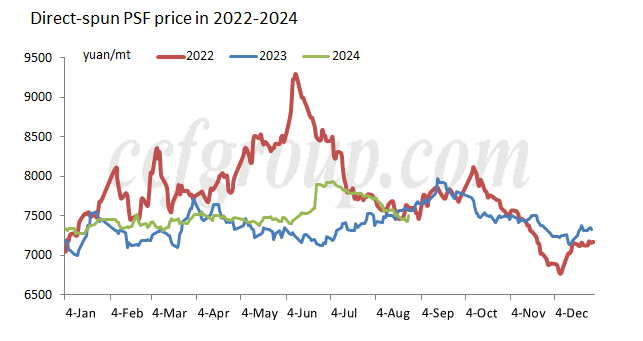

Price: direct-spun PSF prices fluctuated limitedly in the first half year of 2024, within a range of 300-400yuan/mt. From July, as plants supported the processing spread and the financial volatility increased, price fluctuation range expanded to 600-700yuan/mt. Though the fluctuations have increased compared to the first half of the year, they are still relatively small compared to the year of 2022 and 2023. Currently, direct-spun PSF price is in the range of 7,400-7,500yuan/mt.

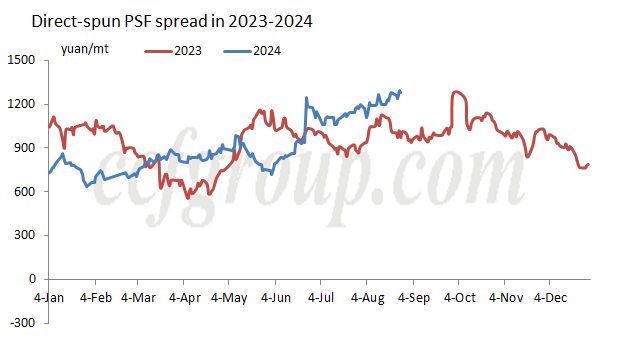

Processing spread: since late June, after plants supported the processing spread, direct-spun PSF spread expanded quickly to 1,100-1,300yuan/mt, a high level in two years. But the high processing spread has been achieved at the expense of operating rate and inventory. Due to lower price, inventory devaluation, high inventory pressure and slow demand recovery in late Aug, some prices soften and sellers provide discounts, to realize the current high processing spread.

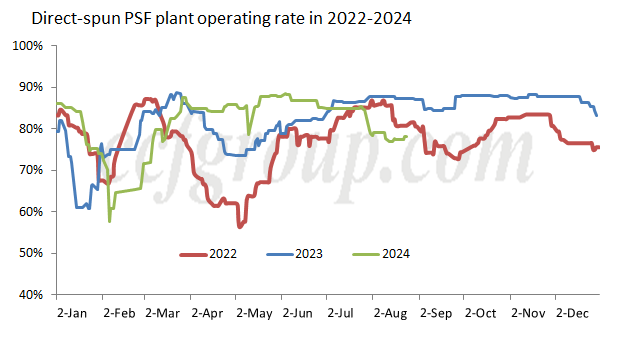

Operating rate: Since PSF plants cut output and maintain the processing spread in late Jul, PSF operating rate remained below 80% in Aug, which is a low level compared to other periods except for the Spring Festival. Compared to last year and the year before, it is also at a low level for this period.

Operating rate: Since PSF plants cut output and maintain the processing spread in late Jul, PSF operating rate remained below 80% in Aug, which is a low level compared to other periods except for the Spring Festival. Compared to last year and the year before, it is also at a low level for this period.

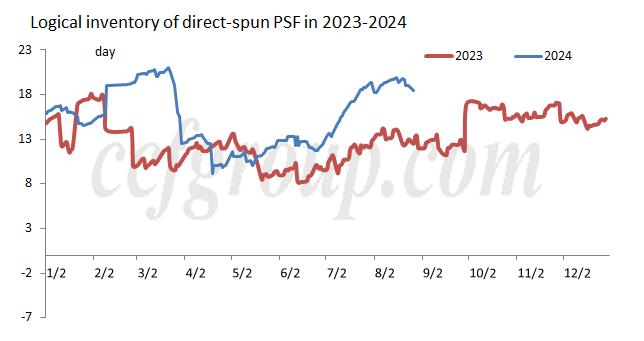

Inventory: In July, the market was in the traditional off-season, and combined with the plants' efforts to maintain the processing spread, inventory quickly increased. In Aug, due to output cuts and downstream replenishment at low prices, the accumulation of inventory slowed down, and a slight reduction in inventory occurred in late Aug. However, inventory remains at a high level for the year, and compared to the same period last year, inventory is also higher.

From the above data on the operation of PSF this year, it can be seen that the market has been relatively stable compared to previous years. Factories have improved their self-discipline, but due to repeated financial issues and expectations of raw material supply surplus, strong market expectations are unlikely to emerge.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price