Nylon 66 market disorder under new capacities

Continued dullness in June-July

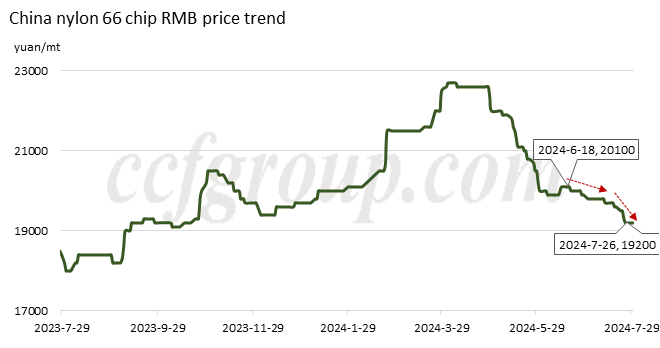

Starting in mid-July, nylon 66 chip market saw an accelerated downward trend, with mainstream chip suppliers further widening their discount on actual transaction prices. The mainstream high prices generally fell below the 20,000yuan/mt threshold, dropping to around 19,500yuan/mt (for bulk orders), while some lower-priced sources fell below 19,000yuan/mt, with some negotiations dropping to between 18,500-18,800yuan/mt.

Previously, from June onward, due to ongoing weak profitability, suppliers initiated a round of price increases. At that time, the lower market prices were around 19,500yuan/mt, while slightly higher prices were between 20,300-21,000yuan/mt. However, due to weak demand, the price increases themselves could not stimulate speculative demand, leading to an overall continuation of weak prices. As July progressed, market returned to a gentle downward trend. By mid to late July, some factories anticipated that August prices would generally decline, prompting them to carry out preemptive low-price promotions, accelerating the downward movement of prices.

Rising supply pressure more worrisome

In fact, beyond the pressure from demand side, the increase on supply side is more concerning. In the early second quarter, after the Tianchen Qixiang resumed operation, the operating rate was relatively high, and the participation of Juheshun had some impact on market prices. In addition, Shanghai Shenma's new 20kt/year facility and Pingdingshan Shenma's new 40kt/year plant were also commissioned in the second quarter. In July, Invista partially launched its new capacities, and it's understood that the new capacity has reached nearly 40,000 to 80,000tons/year. Meanwhile, in June, a 40kt/year plant from China Resources (Huarun) began trial runs, and by July, it had produced high-quality products, with plans to officially quote prices for the market by the end of the month. Considering the previous long-term shutdown of the Tianchen, and the newly commissioned facilities, a total increase of 150,000 to 200,000 tons has been released. This is a significant impact for the nylon 66 market, with its current total demand NOT exceeding one million tons still. And there are still many commissioning plans on the horizon in the coming months.

| Company | Capacity (kt/year) | Time of startup |

| Pingdingshan Shenma | 40 | Q2 |

| Shanghai Shenma | 20 | Q2 |

| Invista | 40-80 | Jul |

| China Resources (Yantai Huarun) | 40 | Jul |

| Anhui Haoyuan | 40 | Aug |

| Shandong Longhua | 40 | Oct |

*The capacity expansion plans in 2024 are not complete or final decided.

In the coming months, Invista's new facility is expected to gradually increase its operating rate in the third quarter. There may be some adjustments to the operation of its older lines, but the overall trend of increasing supply is undeniable. Additionally, Anhui Haoyuan's new 40kt/year facility plans to start trial production in August, and Shandong Longhua's new 40,000 mt line is scheduled to gradually start production in October. If plans go smoothly, there could still be approximately 150,000 mt of additional capacity planned by the end of the year.

Due to the 1-2 months required from feeding and trial runs to stable supply, and considering the recent adjustments in production capacity, the market has been flooded with news of many low-priced sources in recent months, with a higher volume of product supply experiencing batch fluctuations. Additionally, due to fluctuations in the raw material market, the cost conditions for different companies vary, leading to significant price differences and disorder in chip pricing.

With increasing inventory and lowering prices, some capacity plans are also scheduled for shutdown as new facilities are commissioned.

| Company | Product | Capacity (kt/year) | Note |

| Pingdingshan Shenma | Nylon 66 | 40 | Planned 45-day turnaround in end-Jul |

| Tianchen | Nylon 66 | 50 | Planned turnaround in mid-Aug |

Uncertainties on feedstock side

In addition to the numerous new production and shutdown plans in the polymerization segment, the raw material side, particularly HMDA, is also experiencing a lot of variability. On July 25, Invista announced the new contract price for HMDA, lowering it by 1,000yuan/mt to 23,000yuan/mt. The decline in raw material prices has opened up further downward space for nylon 66 chips.

| Company | Product | Capacity (kt/year) | Note |

| Tianchen Qixiang | HMDA | 200 | Planned turnaround in Aug |

| Ascend | HMDA | 200 | Planned to start up in Aug, in Lianyungang, Jiangsu |

| Huashen | HMDA | 180 | Recovered run rate to 70%, may further elevate |

In the future, the intertwining news of new facility startups and maintenance will impact the old patterns. New players in nylon 66 chip circle and existing chip manufacturers also have supply relationships on the raw material side, truly embodying a state of "you within me, me within you." Furthermore, since there are three different production paths for HMDA, enterprises will adopt various strategies and tactics. In the third quarter, the nylon 66 industry is destined to face a chaotic battle.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price