The Blunting of EO/MEG Adjustment: MEG Supply Recovery Lacks Elasticity

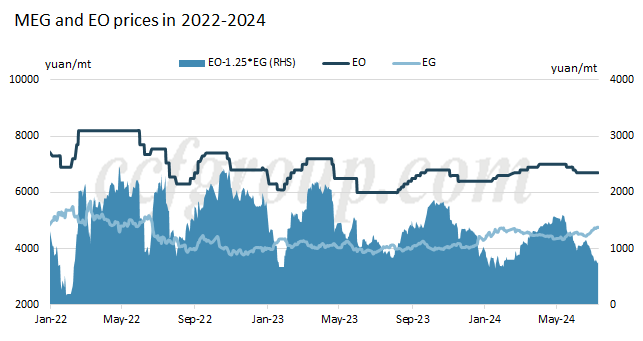

Recently, MEG spot daily average price has risen to 4,750-4,800 yuan/mt, reaching the highest level since July 2022. Despite news of polyester production cuts this week, MEG supply has also decreased. July MEG supply-demand maintains a tight balance, with prices remaining firm.

Boosted by ethylene and MEG markets, ethylene oxide (EO) prices today increased to around 6,800 yuan/mt, with the EO/EG price spread moderately widening to slightly above 800 yuan/mt.

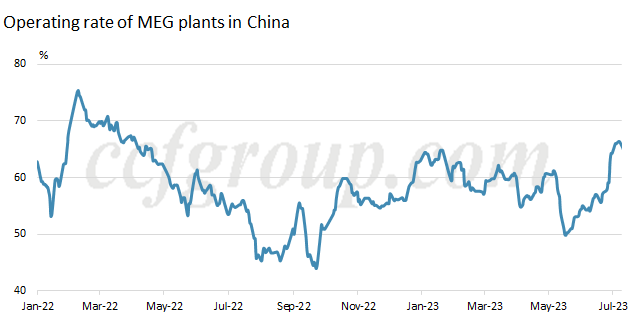

In this round of MEG price increases, integrated plants moderately increased operating rate due to improved margins. However, EO/EG adjustment hasn't responded very quickly. Shenghong's 100kt/year EO unit remains closed after maintenance in early July, diverting ethylene to MEG. Other plants like ZRCC, CSPC, and FREP slightly increased daily production, with expected monthly MEG output increase only around 15,000 mt. Looking ahead, Gulei Petrochemical still has some adjustment potential, but other plants show no clear adjustment plans unless MEG prices rise further and widen the price gap with other ethylene downstream products.

This outcome falls short of previous market expectations when MEG prices rose above 4,700 yuan/mt, as the market was anticipating supply increases from production adjustments.

Undeniably, after years of low MEG prices, companies have been actively upgrading technology and gradually stabilizing. Integrated plants like BASF-YPC, ZRCC, Satellite Petrochemical, and Hengli Petrochemical have undergone EO upgrades and improved downstream EO facilities, extending their industrial chain. As the EO market faces large new capacity releases, it has also undergone internal capacity elimination, such as long-term shutdowns of Shanghai Petrochemical and Yangzi Petrochemical's EO plants.

As for EO external sales, competition among enterprises is intense. Taking Zhejiang as an example, ZRCC, Fund Energy, and Sanjiang Chemical have formed a relatively balanced market with stable sales channels and market shares. Therefore, without sustained significant increases in MEG prices or notable weakening of EO demand, there's limited room for companies to adjust related products.

Against this backdrop, EO/MEG adjustment in integrated plants has become less responsive. Effective recovery of domestic MEG supply still depends on the restart of one of Satellite Petrochemical's lines and the progress of ZPC's rate increase. However, significant increases from this sector are unlikely to be seen in mid-July.

- Top keywords

- Cotton Price

- Cotton Futures Price

- Cotton Futures

- CZCE

- PTA Futures Price

- Chemical Fiber

- Polyester Prices

- Wool price

- PTA Futures

- Shengze Silk

- China

- Yarn Price

- price

- China Textile City

- Fibre Price

- Benzene Price

- Cotton

- Index

- Cotton Index

- PTA

- fabric price

- NYMEX

- Top 10

- textile industry

- Spot Cotton

- Cotton Yarn

- Polyester Price

- Futures

- PTA Price

- cotton yarn price